While there have been some predecessors, inkjet digital production printing truly launched its success story at a European trade show: IPEX 2006 in the UK. The event marked the introduction of the Screen TruePress 520, which was soon taken on by Ricoh/InfoPrint as the InfoPrint 5000. Like several other great print shows IPEX is history, but inkjet digital production printing is here to stay and is taking on an ever-bigger role in the printing industry.

From a worldwide perspective, transaction and related printing applications were the biggest initial market for continuous feed inkjet digital printing due to immediate efficiency gains and ability to add variable colour and TransPromo content. Given the more limited paper choice and print quality of the first inkjet systems, transaction was the best application fit as well. In the years from 2007 to 2010, probably 80% of all CF inkjet installations in Europe went into transaction print or mixed environments. Unfortunately, there are no detailed statistics available on the breakdown of installations by company type.

It might be a surprise that the first countries embarking on colour inkjet were located in Southern Europe, with Italy and Spain leading the installations in the first years, followed by France. Large size users with activities in transaction print in Italy like Postelprint (a subsidy of the Italian post), Selecta and RotoMail and Vesa in Spain invested in multiple print lines early on. Those companies banked on the opportunity colour printing offered in enhancing statements.

After 2010 the installations in the UK and Germany were able to overtake the numbers sold in other countries in Europe – as should be expected given the size of the printing industry and general economy. Focus of these installations was mainly preprint replacement and taking advantage of the higher productivity. Germany remains the most important market for CF inkjet printers for transaction print in Europe today.

The data centre legacy of most transaction printers also had a strong impact on the printer vendor choice, dating back to the time when a billing printer was considered a peripheral to a mainframe computer. Traditionally Siemens mainframe computers had a strong market position in Europe. This gave Océ a head start after acquiring the Siemens high speed printer division in 1996. Ricoh was able to take advantage of the IBM InfoPrint base, but IBM did not have such a dominant market position in mainframes in Europe as it had in the US. French mainframe manufacturer Bull spun off its printer division as Nipson in 1996 as well, but without inkjet solutions this business lost ground. Today Canon-Océ retains a strong market position in Europe, although the vendor choice increased noticeably.

Like in all geographies, transaction printing is under pressure in Europe due to printed documents being switched to electronic alternatives, usually for cost reasons. Despite an ongoing decline in printed billing volumes, transaction printing in Europe remains a large market. There has been less consolidation among companies issuing bills (financial, telco, utility, insurance, governmental, etc.) and the national structure of most institutions is keeping the number of sites up as well.

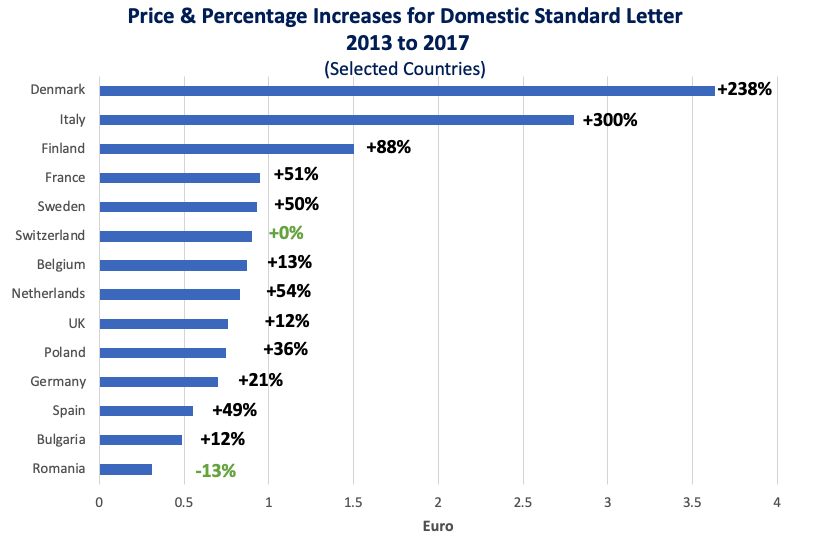

It is easy to overlook how the country dynamics differ in Europe. The Nordic countries are massively pushing electronic document usage and hence are cutting transactional print volumes. The UK is one of the countries with a robust move to outsourcing and centralising print, while most other countries prefer in-house production or sometimes shared print sites. The German speaking countries tend to be more conservative and transaction print volumes have kept up relatively well. Italy however experienced a rapid drop in transaction print based on a massive increase in postal prices.

While the US continuous feed press sales did see a hike in the last two years, the European placements were flat at best. They now represent roughly two thirds of the US placements, despite Europe having a larger population. Another major difference compared to the US is that MICR has almost no importance in Europe.

Moving forward a couple of trends will govern the demand for inkjet printers for transaction printing in Europe

- Some countries will have rapidly declining transaction volumes due to high postal costs and digital document policies. Other countries will remain more stable.

- An increasing volume of regulatory information will mitigate the drop in transaction print volumes. The average number of pages per envelope is increasing.

- Printers are looking into other applications to fill up capacity. This will require other papers, likely a higher print quality and additional finishing equipment.

- Lower cost devices will be preferred. Volumes are coming down, but sites still want multiple lines for backup reasons. There is less pressure to consolidate or move to faster devices as the focus of billers is still on national markets.

- For some of the reasons mentioned above, cut-sheet inkjet will gain importance in the future for transaction print, although the mainstay will remain continuous feed.

While transaction printing still accounts probably for a third of all CF inkjet sales in Europe this portion is about to erode slowly. There is little top-line growth in capacity, but replacement of older devices is lowly kicking in. Other application areas will show a more promising outlook. We will have a look at these market segments in following episodes of this series of articles.

Ralf Schlözer is the EU correspondent for Inkjet Insight based in Berlin, Germany. He brings over 30 years of experience in the Graphic Arts and Graphic System Manufacturing industries with a focus on digital and inkjet. Ralf is a consultant and technology analyst providing insights on technologies, applications, business models and market development. He is also an expert on market sizing and statistical sources around the printing industry.