After offering a look at inkjet’s impact on several packaging segments (folding carton, flexible packaging, corrugated and can printing) this article is covering inkjet in label printing.

Unlike the packaging segments covered previously, digital print is already an established technology in label printing. Labels have proved to be a fertile ground for digital print due to:

- A higher portion of shorter runs than in other packaging markets, as labels are often used in niche markets or where other types packaging print have high set-up costs

- Smaller formats than other package prints – which is easier to achieve by digital print

- A substrate that is generally easier to handle than other types of packaging

Pressure sensitive labels can be produced by almost any digital printer. However, feeding blank label sheets is time consuming, the substrate choice is limited, further processing is more complicated and it is generally not very efficient. Accordingly, most label volume is produced on dedicated roll-fed label printers. Excluding entry level presses, I.T. Strategies reckons in their “Digital Production Label Market – Review of 2020” report that there were almost 4,000 dedicated label printers in use by the end of 2020.

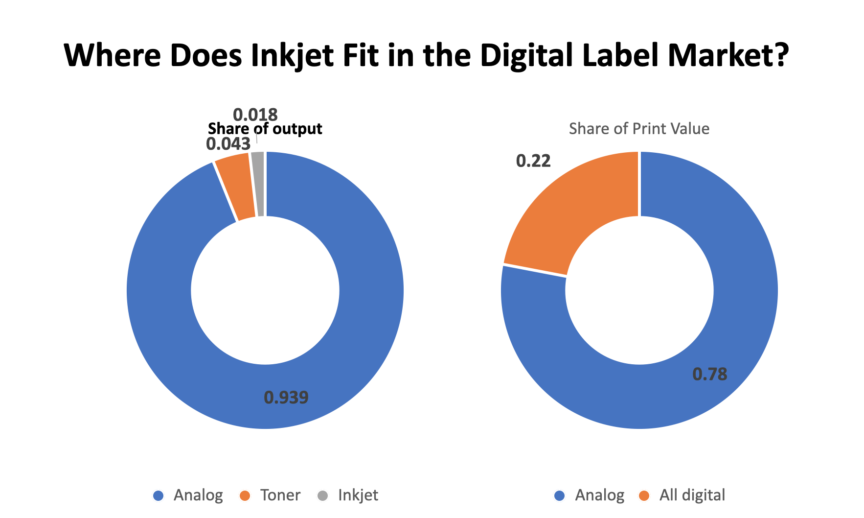

Despite the ongoing investments in label presses, the total share of all pressure sensitive labels printed digitally is still relatively small with just over 6% of all prints. The longer established toner printing is taking the lead in digital volumes with inkjet catching up. Because digital is serving the high margin, short run market the value of the labels produced is much higher. Looking at value, rather than volume, digital has a 22% market share and that portion is forecasted to continue to grow rapidly.

Shares in pressure sensitive label production

Market drivers

Label printing volumes have generally been on the rise in recent years. The Covid-19 pandemic accelerated the uptake among traditional label applications and some new solutions. Labels were an easy solution to attach marketing and product information when supply chains failed and other print was not available. Increasingly labels were used on shipping boxes, to mark products or show last minute changes.

Shorter runs in labels are on the rise, driven by general trends in packaging markets towards more brands, special promotions, test marketing, less inventory and faster reaction on market demand. Upstart and craft producers find an easy entry into product and packaging branding with labels. The market for labels is quite diverse. Apart from prime labels, which convey brand and marketing images, there are secondary labels. Those show mainly informational or logistics content, like IDs, safety information, statutory information or tracking data.

It is also notable that, pressure sensitive labels are growing at the expense of wet glue labels, increasing the pressure sensitive label market overall.

The digital label press market

For the end user the digital printing process should not matter. However, there are quality standards that must be met. Toner print had an early start in this market and set the expectations in quality, especially smoothness and detail.

UV inkjet in labels has not seen the push-back that UV inks get in other packaging markets, due to food safety concerns. This might be down to the lower likelihood of food contact with labels. Secondary labels are less critical as well. Here the high durability of UV inkjet on many surfaces is even a big advantage. UV inks tend be glossier than toner output and can create a raised image. While some end customers prefer the flat toner look, others find the appearance created by UV inks more appealing.

Overall Inkjet has caught up noticeably in recent years in terms of quality, detail rendering and smoothness. Using the new models, the output is generally accepted by brand owners. Aqueous inkjet is promising to close the gap with toner even further.

When considering UV or aqueous inkjet, there is no shortage of dedicated label printing press vendors. More than 20 players offer label printers, often with multiple models in the line-up. Compared to other packaging markets this choice can get bewildering.

Users are well advised to drill down on what a press can offer compared to others. The Inkjet Insight Device Finder can be a good starting point. A first approach in finding the right device is to look at the desired volumes and sturdiness. There are several tiers of devices in terms of productivity (although there are always cases one can argue which is the best fit). We have categorized the market broadly as low volume, mid-high volume, and hybrid.

In my next post, I provide an overview of these categories, the key players in each and a look at where we expect to see new developments.

Editor’s note: as a complement to market and technology overviews, see also label and packaging workflow articles from Pat McGrew.