In my last post, on inkjet in label printing I talked about the benefits packaging print service providers get from digital printing, and why the label sector of the packaging market was the first to adopt digital technologies. In this post, I look at the beginnings of the market to uncover why inkjet adoption has been slow and the potential for the future.

The pioneering Jetrion machines were launched in 2006 (before EFI bought the company). A dozen years later, those machines and their direct descendants claim an installed base in the low hundreds, and have been joined by a slew of competing products from Domino, Durst, Epson, Fujifilm, Heidelberg, Markandy, Nilpeter and many more. These UV-based piezo inkjet machines have been joined by lower-cost, thermal inkjet printers using Memjet technology from companies like Colordyne and Trojan Label. Yet digital printing still accounts for a fraction of the total number of labels printed worldwide – and inkjet printing remains the smaller portion of that digital volume. It’s worth reviewing why this has been so, and in doing so, we’ll see why it’s changing.

What concerns did print service providers (PSPs) serving the tag & label market have, as they considered inkjet technology?

- Reliability & Downtime. Early machines suffered from users’ – and in some cases, vendors’ – unfamiliarity with inkjet technology. They placed machines in environments with paper dust in the atmosphere, with large variations in temperature and humidity, and in the care of operators who were used to cleaning their machines with a rag. As one vendor ruefully said: “You’d better make your printer foolproof, because at some point, it will be operated by a fool.” Some users did not initially have enough work to keep their inkjet printer busy, and learned that printheads do not like to be idle for long periods, even when using non-volatile UV inks. Not all of the reliability issues could be laid at the customer’s door, however. It took vendors a while to appreciate the need for localized environmental control, for automatic head-cleaning, for plug-and-play head replacement, and for the management of static and dust-build up on the web

- Print Quality. The primary quality concern was jet-outs – temporary nozzle failures that cause streaking in the print. These have been largely overcome by the improvements in machine design and working practices described above. The next concern was resolution. The Xaar 1001 greyscale printhead used in many of the early machines printed good-looking photographic images, but its 360dpi cross-web resolution was inadequate for small text. Domino’s adoption of the 600dpi Kyocera printheads forced the competition to ‘double up’ on Xaar heads to get 720dpi, or to move to next generation heads like Fujifilm Dimatix’ Samba head (used in Heidelberg’s product), Ricoh’s ‘Gen 5’ (adopted by Markandy) and others. Another concern was color: traditional printers were used to matching their customers’ Pantone specification with a spot color ink; and they found that the limited gamut of CMYK inks could not always match the required color. The advent of machines that offer OGV (orange, green, violet) color options has – for a price! – mostly fixed this concern. A fourth quality factor was the ink/substrate compatibility referred to earlier. We’ll talk more about this when we come onto flexible packaging, but issues of reticulation (ink drops beading up), the so-called ‘corduroy effect’, and variable gloss all fall into this category of PQ problems.

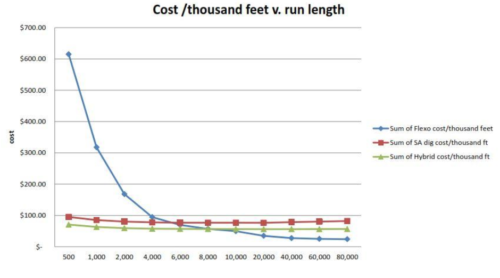

- Cost & Productivity. I bracket these together because every business owner is looking for ROI. Most label printers have a good understanding of the total cost of ownership of their flexo presses, and a hard-won intuition for what any given job will cost to run. But the prospective buyer of an inkjet printer does not have that ‘feel’ for his or her costs. The vendor can produce spreadsheet models, but they rely on assumptions that may not hold true, and take no account of statistical variation. To improve on spreadsheets, it is possible to use simulation software to model various scenarios1 and to generate break-even analyses like this:

1A shameless plug for my own simulation product, PrintSim. If you are interested in customized simulations of analog v. digital manufacturing, use the website or contact Inkjet Insight. - Managing workflow with digital print technology. The primary cause of failure for PSPs adopting any digital technology – whether inkjet or toner – is failure to change the entire workflow of the business. Existing work processes are probably not efficient for small orders. It is a simple fact that 10 orders for 2,000 labels cannot be managed in the same way or at the same cost as a single order for 20,000 labels. Some form of self-service Web-to-Print software for order management is almost essential, as is efficient pre-flighting of customer-supplied files.(A related topic is that sales incentives probably need to change too – salespeople will often ignore low-volume prospects who may be willing to pay a premium for a fast turn-around in favor of a high-volume customer seeking commodity pricing with little margin.)

Another aspect of the label production workflow is one that vendors of digital printers initially ignored: label printing is typically an inline manufacturing process. Die-cutting, foiling, spot varnishing and other finishing processes are usually done on the flexo press. There operations might require a slower run-speed than the press is capable of, but no time penalty is incurred. If the digital printer does no more than print, and the printed roll has to be moved to another machine for die-cutting or what else is needed, productivity is reduced. There are three potential solutions to this, all of which are represented in recent product introductions:

- Add inline die-cutting to the inkjet press e.g. adding a laser cutting unit as in the EFI Jetrion 4900, Durst Tau 330LFS etc.

- Add an inkjet print engine to an existing flexo press e.g. PPSI’s DICEweb, IIJ’s Digital Label Module, or Colordyne’s 3600 Retrofit.

- Create a new ‘hybrid’ machine combining digital and flexo print with finishing. Recent examples are FFEI’s Graphium, Markandy’s Digital Series, and the newly-announced Océ Labelstream 4000.

So, to summarize: inkjet adoption by the label market has been slowed by technical and print quality concerns that have now largely been overcome; by workflow issues that are still extant but for which educational efforts by vendors – forced upon them by an increasingly-competitive marketplace – are helping; and by the lack, until quite recently, of complete inline manufacturing solutions. The presence today of nearly all the traditional ‘heavy iron’ vendors (now including Bobst, with its ‘Mouvent’ venture) supports the belief that (a) the label sector remains attractive, (b) digital offerings are the wave of the future, and (c) for these vendors, this is a stepping stone to the rest of the packaging market.

Chris Lynn of Hillam Technology Partners provides product strategy & business development consulting for technology companies with a focus on digital print and packaging.